Today, enjoy the On the Margin newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the On the Margin newsletter.

Welcome to the On the Margin Newsletter, brought to you by Ben Strack, Casey Wagner and Felix Jauvin. Here’s what you’ll find in today’s edition:

- Felix breaks down possible catalysts for a big run in crypto prices.

- Tokenized funds continue to launch. Here are the latest to hit the market.

- Why fund issuers looking to debut more US crypto ETFs will likely need patience.

What if the bull market in crypto has yet to begin?

Everyone loves to talk about interest rates in nominal terms, but real interest rates don’t get nearly the same attention. Which is a shame, since they could hold the key to understanding the real price drivers behind many asset classes.

Simply put, real interest rates are the market rate of interest subtracted by the market rate of inflation. There are many different ways to measure the market rate of inflation — which is different from economic rates of inflation such as CPI (akin to looking in the rearview mirror).

It’s crucial to pair market data points together. Popular ways to measure the market rate of inflation include market-implied breakeven rates and interest rate swaps, which are more forward-looking, like nominal interest rates.

The 10-year real interest rate measured by the Federal Reserve Bank of Cleveland is one of the better measures of real rates as it combines Treasury yields, inflation data, inflation swaps and survey-based measures of inflation expectations:

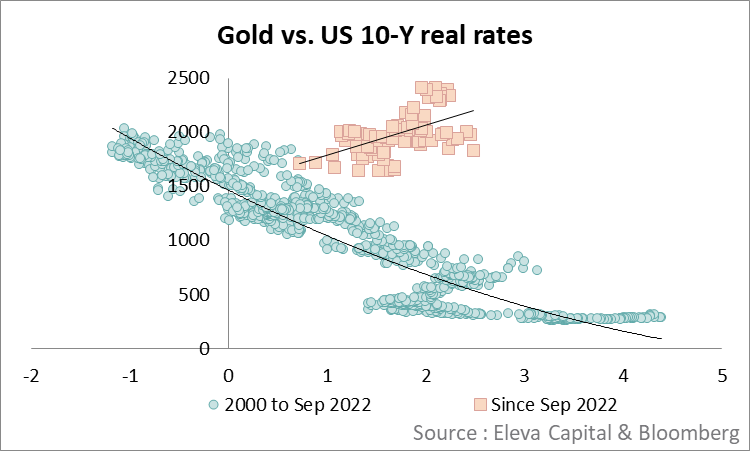

There’s been a long historical negative correlation between real rates and the price of gold that makes intuitive sense. As real rates go lower, the value of the US dollar decreases in real terms. Since gold is a non-yield bearing asset, its relative value increases as the currency it is measured in decreases. Essentially, gold captures the currency debasement caused by decreasing real rates that gets accentuated when real rates go outright negative, as they did in 2020.

What is surprising, however, is how gold has performed through the rate hiking cycle as real rates have increased — we now see a positive correlation occurring as well:

Further, bitcoin has also performed very well in the face of increasing real rates, whilst ultra-risky tech stocks like ARKK (which went up in tandem with bitcoin during the last bull run) have been flat:

Let’s tie all this together:

- Historically, decreasing real rates creates the environment for bull markets for currency debasement assets such as gold and bitcoin.

- For some reason, these two asset classes have been looking past the increase in real rates and are both near all-time highs. Meanwhile, assets that looked like they were of similar risk profiles to BTC, such as ARKK, have flatlined. There are many theories as to why this occurred, from investors hedging against fiscal deficits, to idiosyncratic causes such as central banks buying up gold en-masse and the launch of BTC ETFs this year.

- What can be ascertained from looking at real rates, however, is that BTC looks to be trading more in lock-step with gold, and less with ultra-risky tech stocks. In the same vein, based on the path of real rates in the last two years, a premium for the assets seems to have been baked in, keeping the assets resilient and near all-time highs.

- As the Fed begins its rate-cutting cycle in September, real rates will begin their cycle lower. Moving forward, this will be a major tailwind for returns in both BTC and gold.

In looking at the performances of gold and BTC through the lens of real rates and where they’re destined to go from here, a simple question emerges: What if the real bull market has yet to begin?

— Felix Jauvin

$50 million

The size of the loan crypto lender Ledn has secured from Swiss crypto banking group Sygnum. The syndicated loan is backed by bitcoin, the companies said Tuesday.

Ledn says it will use the capital to expand its retail lending offerings, which have interest rates starting at 11.4%.

Tokenization is all the rage

Hamilton Lane revealed last week that qualified investors can access its new private equity offering (Secondary Fund VI) via a feeder fund available on the Polygon blockchain. The company has enlisted tokenization-focused firm Securitize to help enable this access.

The main draw of the tokenized instrument is the $20,000 minimum investment — substantially lower than the $5 million minimum needed to gain exposure to the main fund.

Secondary PE funds purchase equity stakes from primary investors, usually offering exposure to more mature portfolios. Hamilton Lane’s Secondary Fund VI had its final close in June 2024 with $5.6 billion in commitments, a record for the firm.

It’s the latest tokenized fund to hit the growing market. Securitize this summer also partnered with Investcorp and Arca to bring tokenized feeder funds and tokenized Treasury funds to qualified investors.

New types of products are hitting the market, too. Superstate last month unveiled its Crypto Carry Fund, a tokenized fund that seeks to mimic the “cash and carry” trade in crypto. The fund essentially tokenizes basis trades (when traders buy spot assets and simultaneously sell options).

“An intriguing twist is the potential for the token as collateral,” Noelle Acheson, author of Crypto is Macro Now, said of Superstate’s product. “US Treasurys are collectively the world’s largest collateral asset in [TradFi]; here we have a ‘safe’ token with a higher yield, with the risk largely limited to counterparty issues.”

Tokenized money market funds reached $1 billion in assets under management, according to a June report by McKinsey & Company. Analysts at the consulting firm said they expect tokenized market capitalization across all asset classes to reach $2 trillion by 2030.

Tokenization seems to be a crypto-related topic many traditional asset managers are most interested in exploring, so I certainly expect the market to grow.

— Casey Wagner

The next planned US crypto ETFs are in limbo

The SEC is clearly in no rush to clear the next wave of planned US crypto ETFs.

US spot bitcoin ETFs, check. ETH funds, check. Next up on the docket are (or were) proposed solana offerings and multi-asset products.

The prospect of SOL ETFs seeing approval anytime soon has taken a major turn.

Confirming previous reports, a source familiar with the filings told Blockworks the SEC essentially rejected plans filed by Cboe on behalf of 21Shares and VanEck. The agency appears “of the position that solana is a security and not a commodity,” the person added.

Some segment observers had previously noted the longshot of near-term solana ETFs — citing the SEC’s preference to see a regulated futures market for BTC and ETH. There is currently no such market for SOL.

More likely to gain a green light are the planned funds looking to hold both BTC and ETH, though it looks like the SEC will take its time with those.

Franklin Templeton filed for such a product last week. The so-called crypto index ETF was similar to one filed by Brazil-based asset manager Hashdex in June.

A potential delay in the SEC approving these might be due to the products’ unique structure, said Fineqia International analyst Matteo Greco.

“The SEC has yet to approve a basket product in the form of a digital assets ETF,” he told Blockworks. “This could prompt the SEC to ask additional questions and require further clarification from the issuers before granting approval.”

There’s also the fact that issuers have indicated the potential inclusion of additional crypto assets down the line, Greco noted.

Indeed, Hashdex noted in its June filing that crypto assets meeting certain criteria — such as being listed on a US-regulated platform — could be added to the fund’s index. Franklin Templeton notes a similar possibility.

This prospect is one “potentially leading to more discussions between issuers and regulators,” Greco said.

As for timeline, the SEC delayed its decision on the Hashdex proposal on Aug. 9, noting it would approve, deny or push its ruling again by Sept. 30.

In terms of demand for such funds, diversifying exposures by holding more than one segment asset is generally viewed as a positive, Greco noted.

He added: “This approach is often favored by [TradFi] investors, who aim to reduce risk.”

— Ben Strack

Bulletin Board

- State Street said Tuesday it has partnered with crypto infrastructure provider Taurus. The financial giant plans to tap into Taurus’s custody and tokenization capabilities “to automate the issuance and servicing of digital assets, including digital securities and fund management vehicles,” the company noted in a news release. Stay tuned for more details on State Street’s specific crypto-related priorities.

- Though BTC’s price rose to roughly $61,000 Tuesday morning, it was trading around $59,300 at 2 pm ET — roughly flat from 24 hours prior. ETH had seen a 1.8% decline over that span, trading at about $2,590 at that time.

- In case you missed it, Blockworks editor David Canellis yesterday wrote about how much former President Donald Trump has benefitted from secondary NFT sales and token taxes paid by unofficial memecoins.

Start your day with top crypto insights from David Canellis and Katherine Ross. Subscribe to the Empire newsletter.

Explore the growing intersection between crypto, macroeconomics, policy and finance with Ben Strack, Casey Wagner and Felix Jauvin. Subscribe to the On the Margin newsletter.

The Lightspeed newsletter is all things Solana, in your inbox, every day. Subscribe to daily Solana news from Jack Kubinec and Jeff Albus.

This news is republished from another source. You can check the original article here